Regional report: Asia insights

08 December 2020

Three representatives from IPAF provide an analysis of the MEWP market across Asia.

Bai Ri, IPAF’s representative for China; Jason Woods, IPAF’s regional manager, Middle East and South Asia; and Raymond Wat, IPAF South East Asia regional general manager, each share their views on the development of the access equipment sector in their respective countries and regions.

Extracts from their articles can also be found in Access International’s major new report on the Asian aerial platform sector, which focuses on the challenges and opportunities in key markets throughout the continent.

CHINA

Bai Ri, IPAF representative for China

The estimated total fleet size in China is expected to be around 150,000-200,000 units by the end of 2020, after several years of sustained and rapid expansion. Having mainly been used in ship-building, MEWPs are now widely adopted in construction, municipal and facilities maintenance. Growth rate is estimated to be about 30% a year. As the market matures and competition intensifies, this is expected to slow.

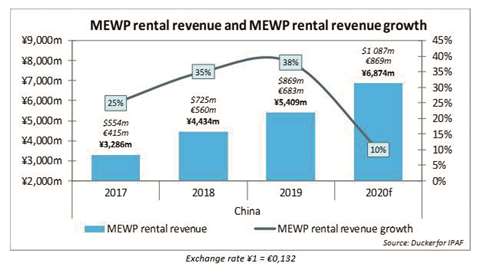

In 2019, the Chinese MEWP rental market value was $853 million, or €802 million, according to the newly published IPAF Global Powered Access Rental Market Report 2020, 2019 was a boom year for China’s MEWP rental businesses, with the strongest growth in MEWP rental value reported over the past five years (around 38%).

The market keeps expanding, new companies entering the market and all players are expanding their fleet in order to meet growing demand. While approximately 800 companies were reported in 2018, the total number of MEWP rental companies in 2019 almost doubled, to stand at around 1,400.

Covid-19 impacted the Chinese market, though to a different degree than in the US or Europe: Activity in China was paused for a shorter time than most other countries at the beginning of the outbreak, with a strict lockdown for less than three months; the market has already returned to something like normal. For SME rental companies, business did slow and many chose to stop investment in fleet expansion or purchase fewer new machines compared to previous years. However, the major rental companies have continued fleet expansion regardless of the Covid-19 situation; Shanghai Horizon alone bought more than 20,000 new MEWPs this year. Overall, fleet growth is similar to last year and the market in China is already recovered and moving forward almost at full speed.

Some small rental companies are having a more tough time; larger rental companies are doing quite well. Rental rates have fallen back as competition is very fierce and increasing all the time. After five years of growing steadily, and the Covid-19 hurdle seemingly cleared, the outlook for the future of the Chinese MEWP rental market is good: The overall fleet is expected to increase further; but the rate of growth is likely to be slower and the competition much more fierce as the market matures.

Demand for operator training remains static but one driver for increased uptake is likely to come from some of the larger multi-national companies that are operating in China, some established players such as JLG are exhibiting growing interest in training. New standards are being planned that will be equivalent to ISO16368.

Boom-type machines offer the greatest opportunity for market growth compared to the other types of MEWPs. Accidents related to powered access are less frequent compared to those involving other construction equipment and scaffolding, which will also be an incentive and driver of continued market expansion.

Training is still to be further developed in this market, and if the price-point for offering high-quality training is correct there is likely to be huge demand for training.

MIDDLE EAST & SOUTH ASIA

Jason Woods, IPAF regional manager, Middle East and South Asia

In the Middle East and South Asia there is a significant and diverse powered access market. MEWPs and MCWPs are extensively used in many industries including aviation, construction, facilities management, oil and gas.

The market was estimated to be growing in terms of fleet size and rental revenue at 5-8% before the coronavirus pandemic struck. Many companies in the Middle East and South Asia report utilisation rates of around 80 to 85% in the high season, and that MEWPs tend to go out on hire for longer periods than other countries projects can be up to 5 years long.

Covid-19 almost stalled the whole industry, thankfully rental companies are starting to recover. In India we are now seeing utilisation rates up to 65-70%, whereas the Middle East is still around 60%. Many rental companies have put safety precautions in place. The market is slowly recovering, construction sites are up and running and borders are starting to re-open.

As a result of the pandemic, many rental companies are going through a re-budget and targets are being revised. This is likely to continue throughout the next six months to monitor and respond to market demand.

In the past five years we have seen a steady climb in demand for MEWPs in the Middle East; India has also seen steady pace of growth. I believe the market will mature thanks to continued steady growth, but it may take some time for significant fleet increase, meaning utilisation rates will likely remain above those typical in Europe or the US.

Training in the Middle East is really well established now and starting to get back on track post-pandemic. UAE has taken the lead with KSA following and IPAF expects to issue around 8,000 PAL Cards for the Middle East across 2020. India is slower on the uptake for quality training, with numbers of trained operators significantly lower than the estimated 6,000 MEWPs in the country’s rental fleet.

Laws and standards that are broadly inline with those in Europe or the US are slowly being adopted in both the Middle East and South Asia. IPAF is involved in helping these standards being implemented; this takes time with a lot of work and research to assist and influence local and regional governing bodies. We expect a new construction standard to be launched in Qatar soon.

Safety is being influenced as there are many MEWPs/MCWPs being used countries coming away from traditional standard way of working reaching out for safer systems of work. The risk from Covid-19 is being addressed and managed, and the focus is starting to shift to how businesses can run safely and efficiently in the post-pandemic environment.

SOUTH EAST ASIA

Raymond Wat, IPAF South East Asia regional general manager

The estimated fleet size of countries in South East Asia region varies considerably, from the mature markets of Korea with 62,000 and Japan at 77,000, Hong Kong (China) 17,000, Singapore (16,000) and Taiwan (11,000) to still developing markets such as Malaysia (7,000), Vietnam (4,500) and Thailand (4,200). Countries that have only recently begun to adopt MEWPs more widely include Indonesia with a fleet size of around 1,500, the Philippines (1,000) and Myanmar (230).

Typical applications include constructions, aviation, oil refinery, facilities management, infrastructure maintenance, and the entertainment industries including film, TV and sports.

Generally during the start of Covid-19 outbreak in January 2020, most of the markets in Asia except Taiwan, Hong Kong and Korea ground to a halt. After the lockdowns were lifted in those countries that imposed one, rental business began to recover but not quite as before with sites tending to have more restrictions around safe distancing. Most countries resumed work after the lockdown, however most countries are now being hit by a second wave, thus markets are slowing down once again owing to the restrictions in place. Safe distancing on job sites is now part of the “new normal”.

We have seen most rental companies increasing their MEWP fleets in all countries across this region during the past five years. The outlook for the future is generally positive, but investment in fleet expansion has slowed for most rental companies in the region.

There has been a significant increase in uptake of IPAF’s MEWP for Managers eLearning training, in part owing to the lockdown. Uptake of operator training in this region is slow.

Nothing significant has changed with regards the regulatory landscape as authorities in this region are busy with dealing with the threat posed by Covid-19, and no new standards are planned. The industry is expected to grow, not least as maintenance and ongoing construction projects need catch up having been paused during the pandemic.

Challenges in the developing markets are typically cost-based; the relative affordability of other access types such as scaffolding, relatively low labour costs and less stringent enforcement of safety measures by the regulating authority can all have restricting effects on the powered access market. It is to be hoped that as economies continue to recover after the pandemic, and the catch-up process begins on the construction pipeline backlog, more contractors across the region will switch on to the benefits to productivity and safety powered access can provide.

STAY CONNECTED

Receive the information you need when you need it through our world-leading magazines, newsletters and daily briefings.

CONNECT WITH THE TEAM