South East Europe optimism

06 December 2017

An optimistic forecast for construction outlook in South Eastern Europe up to 2019 is being slightly tempered by lower expectations about EU fund absorption on the forecast horizon, and only moderate optimism is being seen for Russia, Turkey and Ukraine.

EECFA (Eastern European Construction Forecasting Association) – the forecasting association conducting research on the construction markets of eight Eastern-European countries – has published its 2017 Winter Construction Forecast Reports.

The countries EECFA describes as the South East Europe Five are Bulgaria, Croatia, Romania, Serbia and Slovenia.

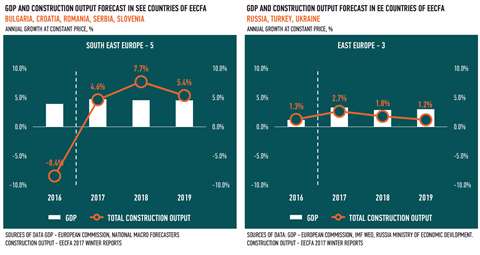

It said the overall picture was still very optimistic given that the whole region was benefiting from the healthy macro environment experienced across Europe, and the record low interest rates.

However, the expansion rate of the total construction market has been revised downwards, mostly because of the worsened expectation in EU fund absorption on the forecast horizon. EECFA said this largely affected the civil engineering submarket, where 9% cumulated growth was foreseen for 2018 to 2019 for the region as a whole.

Favourable

It said that in a very favourable macro environment where money was cheap, building construction was set to continue to recover, with 17% cumulated market growth predicted for the upcoming two years. Shortage of skilled labour in construction was a major constraint on more rapid growth, though, it warned

Bulgaria is facing 7% growth in total construction output in 2017 as EU funds from the new cycle are fuelling civil engineering construction, which dragged down the whole sector in 2016.

Total construction output comes from a very low level, therefore. In 2016, it nosedived by 35.2% – compared to a forecast of 31.1%. In 2018, the construction sector is set to register a 5.6% increase, said EECFA, as opposed to an earlier 6.4% forecast, while 2019 is expected to bring a 5.7% rise, rather than the 4.5% previously predicted.

EECFA said the good news for construction growth in Croatia was the country’s increasing capacity to obtain EU funds, at which the current government seems to be getting better and better.

Continued strong growth in GDP (gross domestic product), private consumption, retail turnover and industrial production should also benefit construction, it added.

Total construction output growth is estimated to be 6.3% for 2017, which has been revised down from the 11.2% growth expected in the summer, primarily as a result of caution shown by buyers, bankers and developers in the residential segment and to delays in some government-led, civil-engineering projects.

It is thought likely that 2018 will bring a 10.9% rise in total construction output, which would be up from the 7.1% expected in the summer, while 2019 should see a 3.9% expansion in this figure. This would also be a rise on the 2.8% estimated in the summer.

The situation with Agrokor – Croatia’s and one of South East Europe’s largest conglomerates which has been facing a huge debt crisis – and has not so far created major problems for the Croatian construction industry, but EECFA said it remained a danger, and if mishandled, could have a strong, negative impact.

The excellent performance of housing and the growth in the non-residential segment in Romania are expected to have counterbalanced low civil engineering outputs in 2017, and to have helped total construction output embark on a 3.6% increase this year. But this is below the 4.3% growth expectations this summer owing to the lower than expected EU fund absorption rates in the first half of the year.

The outlook for 2018 has been revised downwards to a rise of 6.8% – 7.6% was forecast in summer – while 2019 is now predicted to see a larger expansion in construction performance at 5%, instead of the 1.8% expected earlier, as it is thought the civil sector will benefit from new motorway construction works in that year.

Potential for real success

The EECFA said that Serbia’s construction market held a potential for a real success story. Building construction – both new and renovation – showed record highs in 2016 on the back of tailwinds from the permit reform launched in 2015. It said there was a visible convergence of the effects of this permit reform and the economic recovery, which brought along substantial rises in construction across the board.

It added that 2017 would probably witness 3.3% growth, down from the 12.1% predicted in the summer, and 2018 would probably register a 16.3% expansion, up from the 12.9% forecast in the summer. In 2019, the rise will consolidate with an increase of 7.3%, compared to the 9.2% projected in the summer.

EECFA explained that the downward revisions derived from the fact that construction starts of certain big-league projects in the non-residential and civil engineering segments had been delayed, resulting in weaker than expected results in 2017, and stronger growth in 2018.

In 2016, the Slovenian construction slumped by 10.3%, against a predicted 9%, due to the shrinkage of EU funds in the transitory year.

EECFA said the forecast for 2017 was a more cautious 6% now at the end of the year, compared to the 9.6% forecast in the summer.

It said the next few years looked less optimistic now too. In 2018, an 8.2% growth should follow – formerly forecast at 10.1% – whereas 2019 should see a 7% expansion, compared to a 16.1% prediction.

In part, it said, uncertainty came from the civil engineering segment where delays in construction start for two high-volume civil engineering projects would probably not contribute to growth before 2020. Also, downward revisions coming from official data in residential construction values between 2015 and 2018 have changed the picture in the forecast horizon.

Eastern Europe

The East Europe Three in EECFA terms refers to the three large countries of Russia, Turkey and Ukraine.

It said “very moderate optimism” was expressed in the current forecast for the construction market of Russia, Turkey and Ukraine as a whole, as it revised its previous forecast upward.

State intervention and regulatory changes can curb the fall of Russia’s residential market, said EECFA, while civil engineering was expected to perform better than predicted six months ago.

In Turkey, the building construction submarket has been revised upwards moderately. Here the mix of a strong demographic trend, all-time high permit figures and a fragile situation on the financing side have made EECFA cautiously optimistic.

Cumulated growth for the whole region’s building construction is near zero for 2018 to 2019, and civil engineering is forecast to expand 8%. Ukraine is about to outperform region averages on both submarkets, EECFA added.

In Russia, even though a 2.5% shrinkage was foreseen for the whole construction market for 2017 in the summer, it is now estimated to register a growth of 0.3%.

In addition, despite the 0.8% decrease predicted for 2018 and the 0.2% drop forecast in the summer for 2019 in construction in Russia, expectations are now fully positive with a rise of 0.1% for 2018 and 1.8% in 2019.

EECFA said that optimism for the years 2017 and 2018 derived from the awaited increased growth in the civil engineering sector fuelled by new high-volume projects in road and pipeline construction. And the 2019 optimism is based on the fact that the residential segment is likely to be particularly positive, benefiting construction output, fed by an easing mortgage market with low interest rates, legal reforms on new housing and solid housing demand.

The successes of the entire construction sector in 2017 were said by EECFA to be also closely related to the overall improvement of the macroeconomic situation in Russia and the final overcoming of the crisis. The forecast stable development of the national economy in 2018/2019, albeit at a moderate pace, will also be the basis for further growth in the real estate market, it said.

Turkey can be seen as a regional heavyweight as it is still producing the greatest amount of housing – in total floor area – right across Europe.

Third quarter 2017 permit data are showing all-time highs in housing production. EECFA said that this was why forecasts for the whole construction market looked brighter now for 2017 and 2018 than in the summer.

Construction is set to undergo a 4.1% growth in 2017, rather than the 1.4% previously predicted, and should be up 2.8% in 2018, instead of 0.8%. In 2019, only a 0.5% growth could be predicted for the construction market, said EECFA, instead of a 1% rise forecast in the summer. This is because general and local elections will be held that year, and rising construction costs may lead to reduction in demand.

In Ukraine, considerable growth in construction market indicators registered throughout 2017 suggests that the industry has weathered the crisis and is on a development path, said EECFA.

Construction turned out to be the fastest growing industry of the Ukrainian economy in 2017 as a result of a major hike in road construction, the improvement in the financial condition of several industrial players, and the increase in investments.

All this was said to have led to a significant upward revision in construction output in the country for 2017, from 7.7% predicted in summer to 15.7% expected now.

Expectations for 2018 are also better with a 10.1% growth projection in construction instead of the 8% awaited in summer, while for 2019 a decelerated growth of 5.8% should occur, which is lower than the 7% expansion expected in summer.

STAY CONNECTED

Receive the information you need when you need it through our world-leading magazines, newsletters and daily briefings.

CONNECT WITH THE TEAM